Problem: Justine is within medical college and you may intentions to ultimately practice medicine in identical area. She would prefer to own a house and then have the lady lifestyle become, however, do not want in order to if you are she actually is in school. The woman parents are using this lady lease and you will feel just like it is currency lost. They’d will just buy her a house and present they to their, however, would not want current/estate tax effects.

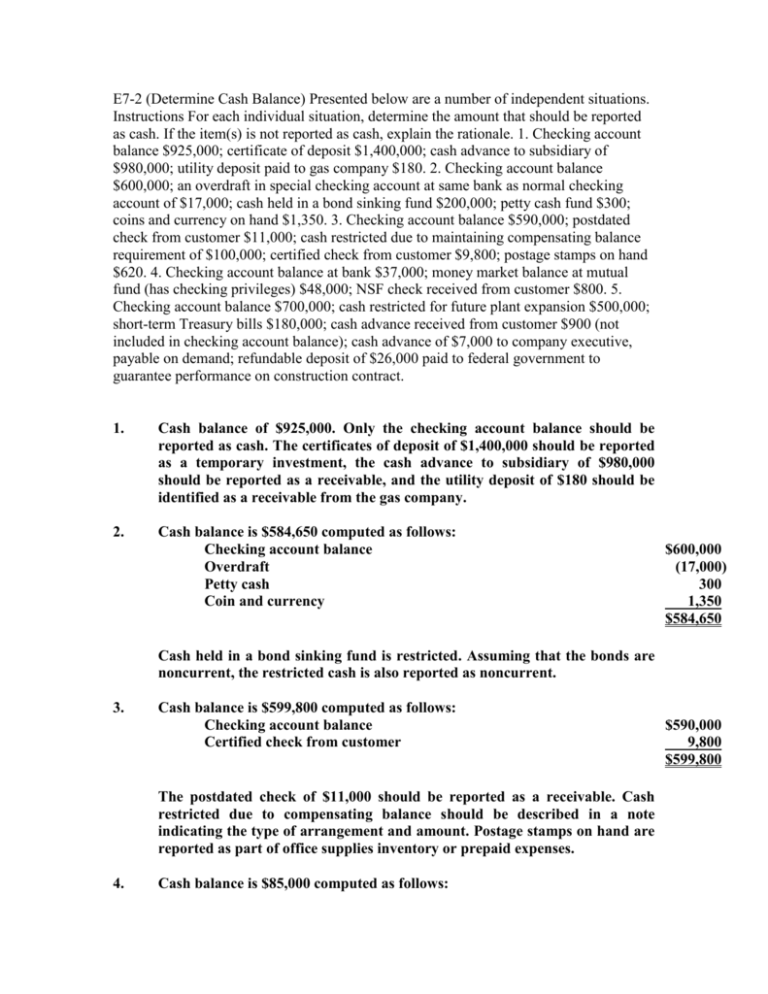

Solution: Justine’s parents find yourself purchasing a house in town where she life, that having an additional room that they’ll remain in when it check out. Yearly, they give their a share off ownership in the home equal in order to $twenty eight,one hundred thousand ( $fourteen,one hundred thousand for every parent) up to Justine at some point possess the entire family. While they for every single remain according to the $fourteen,one hundred thousand annual current income tax exception to this rule, their gradual gifting of the home in order to the girl cannot clean out the newest $ten.nine million existence exception to this rule ($5.45 billion individual) he or she is permitted to gift/give without triggering present otherwise home taxation.

In these items, the term loan try thrown doing fairly easily without much defined as from what financing most mode

Problem: Kevin is within his mid twenties that is intent on to purchase a property. Really the only family he are able is in an adverse society, but they are ok with this. Their mothers must help your away, but don’t need to funds an adverse decision. They don’t get that much cash on hands anyhow.

Solution: Kevin’s mothers choose your finest provide they can provide your is considered the most education. They sit and you can explore his choices and you may introduce him in order to a real estate agent who rationally assesses his package. The real property elite shows you it is extremely unlikely one to he will manage to flip a property for the a bad neighborhood through to the high costs activate. And, it is really not installment private loans London likely that Kevin will receive enough collateral about home at that time, particularly if the worthy of decreases, in order to refinance they. Instead, Kevin ends up to buy a little beginner house in the a beneficial neighborhood and you may plans to generate renovations that may help the worth.

Loaning money having a down payment toward a home is probably first of all comes to mind when you’re thought throughout the permitting children aside having a home.

For individuals who indeed be prepared to get paid straight back, or even to at the very least formalize the newest act of your own loan, or perhaps to merely protect your own connection with your child, you will need to perform an appropriate document one to creates new regards to the loan and you can a cost plan. In that way, your not only provide you with reduced, but you can set up a steady stream of cash that have a share speed which is less than exactly what a bank carry out charges but higher than everything you could get on the a good investment.

The biggest problem you to mothers deal with is actually providing their infants to invest right back new finance as well as the resulting resentment you to definitely adds up because of low-cost out-of funds

- The satisfaction of going your child into the a house.

- An excellent method if you would like disregard the came back to own old age.

- Best for a young child just who seems you to a large gift manage give his or her parents a managing reason for his otherwise the woman existence, is simply too stressed, or simply does not want to feel indebted to the parents.

- For the loaning the cash, the attention could be more than just a grandfather manage log on to an investment however, lower than the kid might be paying to the a home loan. Naturally, this is exactly a thing that might be talked about that have an income tax certified.